Going through a divorce is one of the most stressful experiences anyone can face, and protecting your finances during the process is absolutely critical. Many people focus on the emotional side of things and end up making costly financial mistakes that follow them for years.

Whether you have a lot of assets or just a few, knowing how to safeguard what you have worked hard for can make a huge difference. Here are 18 strategies that can help you come out on the other side in a much stronger financial position.

1. Prenuptial and Postnuptial Agreements

Signed before or during a marriage, these contracts might feel awkward to bring up, but they are one of the smartest financial moves you can make. A prenup or postnup clearly defines which assets stay separate and how future earnings or inheritances get handled.

Entrepreneurs and anyone with significant savings especially benefit from having these in place. Courts generally uphold them when drafted correctly, giving you real legal protection when it matters most.

2. Know the Difference Between Marital and Separate Property

Not everything you own is automatically up for grabs in a divorce. Assets you brought into the marriage or received as gifts and inheritances are typically considered separate property and may stay with you.

Marital property, on the other hand, includes most things acquired during the marriage and is subject to division. State laws vary significantly, so understanding whether your state follows community property or equitable distribution rules is a crucial starting point.

3. Document Gifts and Inheritances With a Clear Paper Trail

Receiving an inheritance or a financial gift during your marriage does not automatically make it marital property, but you need solid documentation to prove it. Keep legal statements, valuations, and transfer records organized and easily accessible.

One major pitfall to avoid is mixing those funds with shared accounts. Once inherited money gets deposited into a joint account, courts may treat it as marital property.

Keeping it separate from day one protects its status throughout any legal proceedings.

4. Maintain Separate Bank and Brokerage Accounts

Keeping accounts solely in your name for assets you consider separate property creates a cleaner financial boundary. When funds get mixed together over the years, untangling them during divorce proceedings becomes expensive and time-consuming.

If possible, label accounts clearly and avoid using them for shared household expenses. This simple habit can save you a great deal of legal headache.

Financial clarity does not just help in a divorce; it also makes everyday money management much easier.

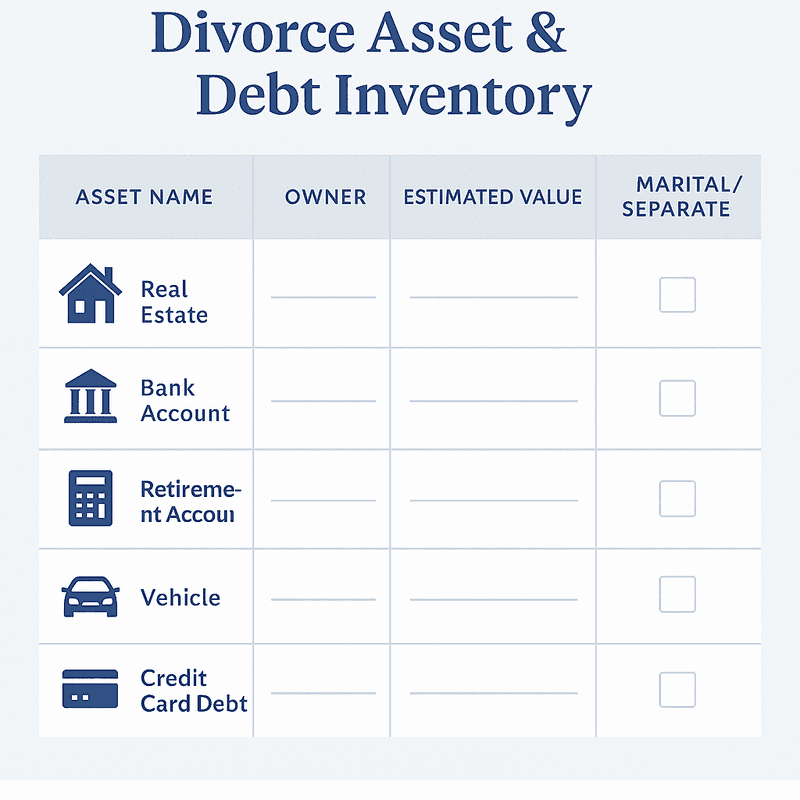

5. Build a Comprehensive Inventory of All Assets and Liabilities

Before negotiations even begin, you need a complete picture of everything you own and owe. That includes bank accounts, real estate, vehicles, business interests, retirement funds, stock options, and even deferred compensation.

Liabilities matter just as much as assets. Joint mortgages, lines of credit, and business loans all factor into the final settlement.

A thorough inventory prevents surprises and gives your legal team the foundation they need to negotiate effectively on your behalf.

6. Organize All Financial Documents Before Proceedings Start

Tax returns, pay stubs, mortgage statements, investment records, and insurance policies all become critical evidence during divorce. Gathering copies of everything before legal proceedings begin puts you in a far stronger position.

Your spouse may have access to joint accounts and records now, but that access can become restricted once proceedings start. Securing copies early means you will not be scrambling later.

Store digital backups in a secure, private location that only you can access.

7. Update Estate Plans and Beneficiary Designations Promptly

Divorce proceedings can drag on for months, but your beneficiary designations on retirement accounts and life insurance policies do not update themselves. If something happens to you before the divorce is finalized, your assets could go directly to your soon-to-be ex.

Review and update wills, trusts, powers of attorney, and account beneficiaries as soon as possible. Some states automatically revoke spousal designations upon divorce, but many do not.

Taking action early rather than assuming the law will protect you is the safer approach.

8. Get Professional Valuations for Complex Assets

Privately held businesses, real estate portfolios, artwork, collectibles, and stock options are notoriously difficult to value without expert help. Guessing or using rough estimates can cost you thousands in a settlement.

A certified business valuator or licensed appraiser brings credibility and accuracy that holds up in court. Both spouses may bring in their own experts, so having a qualified professional in your corner ensures you are not shortchanged.

Accurate numbers lead to fairer outcomes.

9. Keep Business and Personal Finances Completely Separate

Business owners face a unique challenge in divorce because a poorly managed company can easily become a marital asset. If you regularly use business funds for personal expenses or skip paying yourself a real salary, courts may view the business as shared property.

Maintain separate accounts, pay yourself consistently, and document every transaction carefully. Good financial hygiene here does double duty: it protects your business in a divorce and makes your company look more credible to investors and lenders as well.

10. Create a Forward-Looking Budget and Cash Flow Plan

Life after divorce looks financially very different from life during marriage. Housing costs, tax filing status, and income structures all shift, sometimes dramatically.

Building a realistic budget before the settlement is finalized helps you negotiate from a position of knowledge.

Factor in potential spousal support, investment income, and new living expenses. A certified divorce financial analyst can model different settlement scenarios so you understand the long-term impact of each option.

Making informed choices now prevents financial regret later.

11. Establish Independent Liquidity and Access to Funds

Shared bank accounts can be drained quickly once a divorce becomes contentious. Opening individual banking and cash management accounts early ensures you have access to money for everyday expenses, legal fees, and unexpected costs.

Consider closing or limiting access to joint credit cards as well. You do not want to be held responsible for charges your spouse makes during proceedings.

Establishing financial independence early is not just a protective measure; it is also an empowering first step toward rebuilding your financial life.

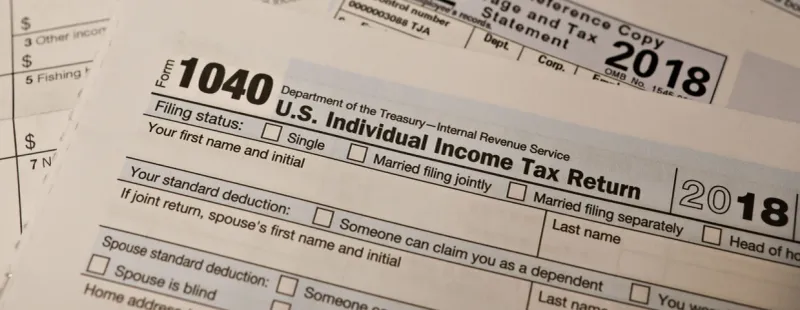

12. Understand the Tax Implications of Asset Division

Splitting assets sounds straightforward until the tax bill arrives. Selling stocks, real estate, or options to divide proceeds can trigger significant capital gains taxes that reduce the actual value of what you receive.

Spousal rollovers and direct transfers can minimize immediate tax liability when handled correctly. Child and spousal support payments also carry specific tax rules that changed significantly in recent years.

Working with an accountant who understands divorce taxation helps you avoid costly surprises when filing your first post-divorce return.

13. Use Qualified Domestic Relations Orders for Retirement Accounts

Retirement accounts like 401(k)s and pensions cannot simply be split with a regular court order. A Qualified Domestic Relations Order, or QDRO, is a separate legal document required to divide these accounts without triggering early withdrawal penalties or immediate tax consequences.

Getting the QDRO right matters enormously. Errors in the document can delay the transfer for months or result in unexpected tax bills.

IRAs follow slightly different rules, requiring clear language in the divorce decree itself rather than a separate QDRO.

14. Assemble a Strong Professional Team Early

Trying to navigate a high-asset divorce alone is like performing surgery on yourself. You need a divorce attorney experienced in complex financial cases, a certified divorce financial analyst, and a tax professional who understands the nuances of asset division.

For business owners, adding a business valuation expert to the team is also wise. Yes, professional fees add up, but the cost of a bad settlement far outweighs the investment in expert guidance.

The right team pays for itself many times over.

15. Never Hide Assets, But Know What You Are Owed

Deliberately hiding money or assets during divorce proceedings is not just unethical; it is illegal. Courts take financial fraud seriously, and getting caught can result in penalties, loss of assets, and a damaged credibility that hurts your entire case.

The smarter play is full transparency on your end while ensuring your attorney conducts thorough discovery to confirm your spouse is doing the same. Forensic accountants can uncover hidden accounts, underreported income, and suspicious asset transfers that might otherwise go unnoticed.

16. Plan a Strategy for Business Buyouts or Asset Offsets

If you own a business and want to keep it, giving your spouse a larger share of other marital assets in exchange is a common and practical strategy. This kind of offset negotiation keeps the business intact while still achieving a fair division overall.

Alternatively, buying out your spouse’s share directly is another option if you have the liquidity to do so. Either approach requires an accurate business valuation to ensure the exchange is truly equitable.

A poorly structured deal can leave either party feeling shortchanged for years.

17. Review and Update Insurance Policies Post-Divorce

After a divorce is finalized, your insurance coverage needs a thorough review. Homeowners, auto, life, and disability income policies may still list your ex-spouse as a beneficiary or co-owner without you even realizing it.

Updating these policies protects your assets and ensures payouts go to the people you actually intend to benefit. Health insurance coverage also changes after divorce, especially if you were on a spouse’s employer plan.

Getting ahead of these updates avoids gaps in coverage at a vulnerable time.

18. Watch Out for Overlooked Assets Like Stock Options, Crypto, and Loyalty Points

Some of the most valuable assets in a divorce settlement are the ones nobody thinks to mention. Unvested stock options, restricted stock units, cryptocurrency holdings, health savings accounts, and even frequent flyer miles earned during the marriage can all be considered marital property.

Accrued vacation time, deferred compensation, intellectual property royalties, and prepaid deposits are other easy-to-miss items. Running a thorough checklist with your financial advisor ensures nothing slips through the cracks and that you receive everything you are entitled to.